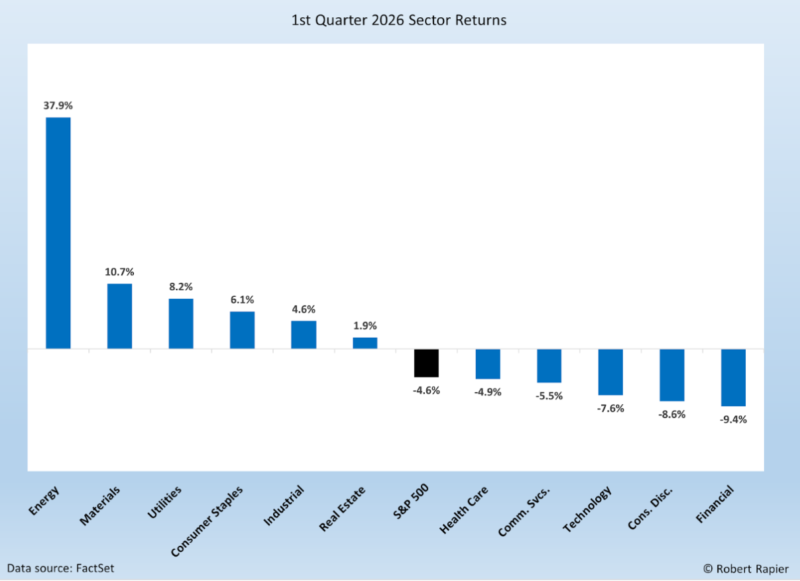

The first quarter of 2026 marked a sharp shift from the broad-based strength that closed out last year. The S&P 500 finished in negative territory as investors wrestled with a new war in the Middle East, stubborn inflation, shifting interest rate expectations, and uneven earnings across major industries.

But the headline decline doesn’t tell the real story.

What stood out in Q1 was the extraordinary divergence beneath the surface. A handful of sectors delivered strong gains, while the broader market struggled. The gap between winners and losers was one of the widest we’ve seen in years—and it reinforced a key theme for investors: sector selection mattered far more than overall market direction.

Energy was the clear standout, surging nearly 38% for the quarter. Tight global supply, strong refining margins, and persistent geopolitical risk kept crude prices elevated and cash flows strong across the sector. This wasn’t a speculative rally—it was driven by fundamentals.

Across the energy complex, every major subsector participated in the rally. Midstream, exploration and production (E&P), integrated majors, and refiners all posted strong gains. But the drivers weren’t uniform. Some benefited from rising volumes and tariff growth, others from direct exposure to higher commodity prices, and a few simply saw long-overdue re-ratings as investors began to recognize just how much cash these businesses are generating.

As always, the returns discussed below reflect total returns, including dividends.

Upstream

According to data provider FactSet, pure oil and gas producers posted an extraordinary average gain of 45.0% in Q1.

Of the 40 upstream companies in the S&P 500, 38 finished in positive territory, and three posted triple-digit returns. The combination of higher commodity prices, disciplined capital spending, and aggressive shareholder return policies created a powerful setup.

Kosmos Energy led the group with a staggering 206% gain, while ConocoPhillips, the largest upstream player, returned 42.1%—in line with the sector average. In short, the rising tide of oil prices lifted nearly all boats during the quarter.

Midstream

Midstream companies—pipelines, processors, and infrastructure operators—also delivered broad-based gains. Most names posted double-digit returns, with only a handful lagging in the single digits. This is exactly the kind of environment where midstream tends to shine: volumes are steady, pricing is supportive, and balance sheets are far stronger than they were a decade ago.

As a group, midstream gained 27.2% in Q1. Tanker companies once again stood out. Tsakos Energy Navigation, Nordic American Tankers, Frontline, DHT Holdings, and Scorpio Tankers all posted gains above 45%, driven by strong day rates and tight vessel supply. The combination of constrained fleet growth and steady global trade created a powerful tailwind for marine transportation.

Downstream

Refining continues to be one of the most compelling stories in energy, and Q1 extended that trend, particularly for the largest U.S. independent refiners. The “Big Three” generated an average return of 48.6% for the quarter, supported by structurally tight global refining capacity.

Valero Energy led with a 52.7% gain, followed by Marathon Petroleum at 50.9% and Phillips 66 at 42.3%. These companies are benefiting from a global system where more capacity has been retired than added, giving remaining operators unusually strong pricing power and sustained margin support.

Integrated Supermajors

The integrated giants also turned in their strongest quarterly performance in years, averaging 36.9%. ExxonMobil led with a 41.9% return, followed closely by TotalEnergies at 40.6%. Strength across the value chain—upstream production, refining, and chemicals—combined with disciplined capital allocation and robust shareholder return programs drove results.

Investors are increasingly rewarding these companies for something that wasn’t fully appreciated a few years ago: diversified cash flow streams backed by some of the strongest balance sheets in the sector’s history.

Looking Ahead

After a quarter like this, the obvious question is whether energy can continue to lead—or whether we are closer to the end of the run.

Fundamentally, the setup remains constructive. Global supply is tight, spare capacity is limited, and years of underinvestment continue to constrain the system. Midstream volumes are solid, E&Ps remain disciplined, integrated majors are generating substantial free cash flow, services are regaining pricing power, and refiners are operating in a structurally favorable environment.

That said, risks are building. The conflict in the Middle East remains a major wildcard. A meaningful global slowdown would pressure demand and compress margins. A shift in interest rate expectations or a broader risk-off move could also weigh on the sector after such a strong run, even if underlying fundamentals remain intact. And at the individual company level, expectations are now significantly higher than they were just a year ago.

For now, Q1 2026 stands as a textbook example of what happens when a capital-constrained sector with improving fundamentals comes back into favor. Energy didn’t just outperform the market in Q1, it defined it.

Keep In Touch with Shale Magazine

As the new era of energy unfolds, you can bet we’ll be the boots on the ground to keep you informed. Subscribe to Shale Magazine for sharp insight into the arenas that matter most to your life. And don’t forget to listen to our riveting podcast, The Energy Mixx Radio Show, where our very own Kym Bolado interviews the most extraordinary thought leaders, business innovators, and industry experts of our time.

Subscribe to get more posts from Amanda Jenkins